By continuing to browse the site you are agreeing to our use of cookies. For more details about cookies and how to manage them, see our cookie policy.

Close to core markets

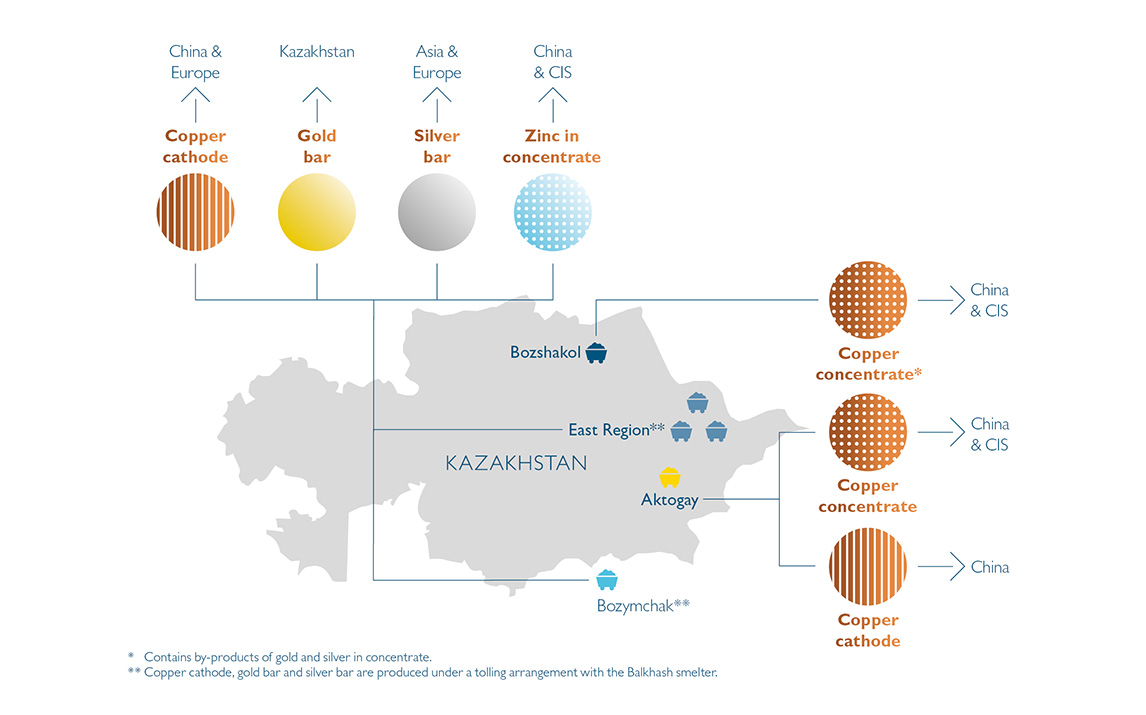

The Group’s revenues are primarily derived from the sale of copper, with additional revenues from by-products of gold, silver and zinc. The Group’s performance is therefore dependent on commodity prices, which reflect global supply and demand fundamentals, as well as market sentiment and the activities of financial investors. Commodity prices can be volatile and cyclical as a result of dependence upon geopolitical and macroeconomic factors. The outlook for the Chinese economy is of particular significance as it is the largest consumer of copper and the main physical market for the Group.

Copper has excellent electrical and thermal conductivity, which makes it essential for all modern infrastructure, energy generation and transmission, transportation, communications, industrial machinery and electrical appliances. Construction and electrical network infrastructure are the two most significant sources of copper demand, and it is therefore a key product in supporting the continued urbanisation of Asia and Africa.

Consumer products, which include air conditioning and refrigeration, are also important sources of demand for copper, which may increase as developing countries transition towards consumer-led growth.

Copper also plays a key role in assisting the energy transition, as the world moves towards low carbon energy generation and low emissions transportation, and there may be higher demand for the metal to support countries in meeting decarbonisation targets. Solar and wind power, and the adoption of electric vehicles with their associated charging infrastructure, are highly copper intensive.